Week 5 (Special Edition) | The Missing Chapter | Joshua Grass, CFA, CFP®

I was recently invited to speak to a group of young engineers, most of them a year or two into their first real jobs. They had come prepared with a written list of questions. Near the top: How do we find a good financial advisor?

Before I answered, I thought about what was really behind the question. Reading between the lines, from the questions they were asking and what they weren’t quite saying, a few things were clear: some felt like they were probably leaving money on the table, some were starting to earn real money and had no plan for it, and more than a few had heard stories about advisors taking advantage of clients and weren’t sure who to trust.

That last part is worth pausing on, because it’s the right instinct. The financial advisory industry has not always been transparent about how it works or how its incentives are structured. The stories people have heard aren’t all fabricated. Being skeptical of someone who wants to manage your money is not paranoid. It’s reasonable. The question is how to channel that skepticism productively, so it helps you find the right person rather than keeping you from working with anyone at all.

The best place to start is the same place I started with those engineers: understanding how advisors make money.

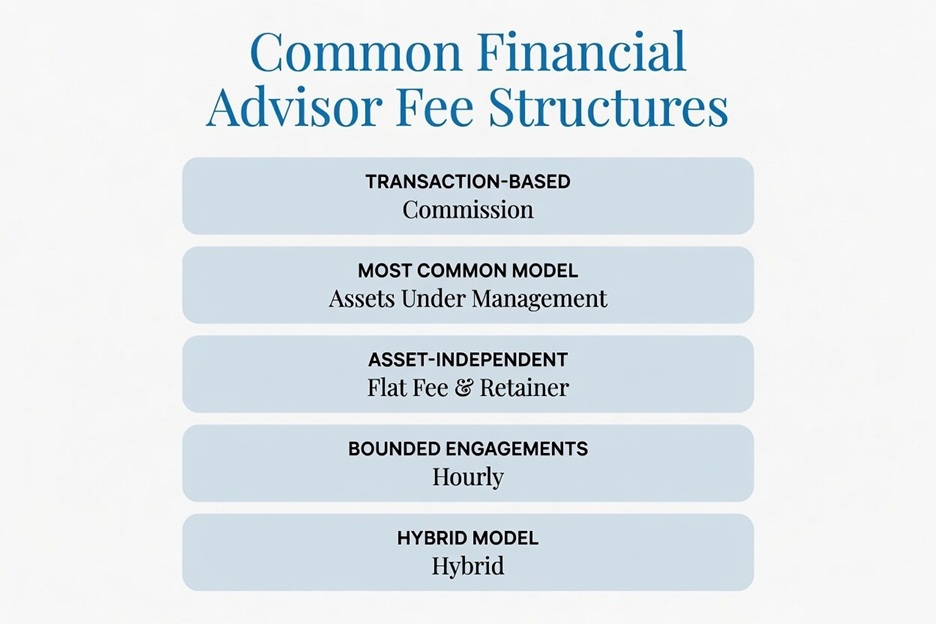

How advisors get paid

The financial advisory industry has several distinct compensation models, and the one your advisor operates under shapes the entire relationship. Here’s what each looks like.

Commission-based. The advisor earns money when you purchase a financial product, a life insurance policy, an annuity, a mutual fund. The client usually doesn’t write a check; the company whose product is sold pays the advisor directly. This is the model behind most of the horror stories people have heard, and it’s worth understanding why: the advisor gets paid when a transaction happens, and paid differently depending on which product is sold. That creates a structural question about whether any given recommendation exists because it’s right for you or because of what it pays.

That said, commission-based advisors aren’t a monolith of bad actors. The model remains legitimate and common, particularly in insurance, where an advisor who helps a young family get the right life insurance policy in place is providing real value and earning a commission for doing so. The model works best when it’s transparent, when there’s a real planning need behind the recommendation, and when the relationship doesn’t end the moment the commission is earned.

Assets under management (AUM). This is the dominant model today. Industry research shows 86% of advisory firms use AUM fees as their primary compensation method. The advisor charges an annual fee calculated as a percentage of the portfolio they manage for you, typically somewhere between 0.5% and 1.25% depending on portfolio size and the scope of services. Fees generally decrease as your portfolio grows.

To make that concrete: on a $500,000 portfolio at 1%, you’d pay roughly $5,000 a year. At $1 million, the percentage often drops; at 0.9%, that’s $9,000 annually. At $2 million, you might be closer to 0.8%, or $16,000 a year. It’s worth knowing that this fee typically covers more than investment management. On average, about 41% of an AUM fee goes toward financial planning and advisory services beyond managing the portfolio.

Flat fee and retainer. A growing number of advisors charge a set annual or monthly fee regardless of how much you have invested, often somewhere between $3,000 and $10,000 per year for a comprehensive planning relationship, though this varies widely. This structure makes the cost predictable and keeps the advisor’s compensation independent of your portfolio size. It’s particularly relevant for high earners who have real financial complexity but haven’t yet reached the asset thresholds that most AUM relationships require.

Hourly. Some advisors bill by the hour, similar to an attorney. This works well for specific, bounded questions: a one-time review of a plan you’ve already built, an evaluation of a job offer’s benefits package, a second opinion on a financial decision you’re weighing. It’s a low-commitment way to access professional advice when you need it. The limitation is that it doesn’t lend itself to the proactive, ongoing relationship that catches things before they become problems.

Fee-based (hybrid). This is worth flagging because the name causes confusion. “Fee-based” advisors charge clients directly but can also earn commissions on products they recommend, meaning they operate in both worlds. “Fee-only” means no commissions at all, full stop. Both can represent excellent advisory relationships, but they’re structurally different, and it’s worth asking a fee-based advisor to explain exactly how they’re compensated for each thing they might recommend.

The legal question most people never ask

Alongside compensation, there’s a second question that’s just as important: Is this advisor a fiduciary?

Most people don’t ask this. They should.

A fiduciary is an advisor who is legally required to act in your best interest, not just when making a specific recommendation, but throughout the entire relationship. They have to put your interests ahead of their own, disclose conflicts of interest, and where conflicts exist, manage or eliminate them. Registered Investment Advisors (RIAs) are held to this standard under federal law.

Advisors who operate as broker-dealers, which includes many commission-based and fee-based advisors, are held to a different standard called Regulation Best Interest, established by the SEC in 2020. This requires them to act in your best interest when making a recommendation, which sounds identical to the fiduciary standard but differs in a few important ways: the obligation kicks in at the point of a transaction rather than running continuously; it requires disclosure of conflicts but not necessarily their elimination; and “best interest” under this standard is legally more subjective and harder to enforce.

The practical difference: a fiduciary is obligated to think about your interests at every step. Under Regulation Best Interest, the focus is on individual recommendations rather than the full ongoing relationship.

So ask: Are you a fiduciary? And then ask the follow-up that matters just as much: Does that apply to everything you do for me? Some advisors are fiduciaries for part of their practice and not others. If the answer is “it depends,” that’s worth understanding before you go any further.

Now, what do you actually want?

With the landscape in front of you, here’s the question that determines which of these models is right for you: What are you actually looking for from an advisory relationship?

Some people want a transactional relationship: help with a specific product or decision, no ongoing engagement, clean and contained. That’s a legitimate preference, and there are advisors built for exactly that. Others want a comprehensive, ongoing partnership: someone actively watching their full financial picture, catching things they’d miss, and staying engaged through major decisions and changing circumstances. That requires more from both sides and comes with a higher ongoing cost.

Knowing where you are on that spectrum helps you match yourself to the right model, and helps you recognize quickly when a conversation is going in the wrong direction.

What good fit actually looks like, and how to recognize the opposite

There’s a reason you wouldn’t take a gas-powered car to an electric vehicle mechanic just because it has a battery. Yes, there’s overlap in knowledge, but the expertise doesn’t fit the problem. You’d likely overpay for specialized skills you don’t need, and the issues you actually need solved may go unnoticed or misunderstood. Finding the right advisor works similarly.

The standard that applies across every compensation model is the same: transparency about who they work with and why. A good advisor should be upfront about what they do, who they’re built to serve, and what a relationship with them actually looks like in practice. That holds whether they work on commission, charge AUM fees, or operate on a flat retainer. The model matters less than whether the advisor is honest about the fit.

Here’s what happens when that honesty is missing.

A client I now work with told me she had opened an investment account some years earlier with another advisor. At the time, she’d saved about $10,000 outside of her work benefits and told the advisor she wanted to put it toward retirement. By any modern standard, that amount doesn’t offer much to an advisor in terms of monetary value. But she found one, and the advisor did something with it.

What got opened was a variable annuity, carrying a 2.5% annual fee. A commission was earned. And then the relationship ended.

Three things made this the wrong product for her.

Timing, first. Variable annuities are designed for the distribution phase — when you’re converting accumulated wealth into income and protecting against the risk of outliving it. At 40, she was in the accumulation phase. The product’s core features — guaranteed lifetime withdrawals, death benefit provisions, longevity protection — are most valuable when you’re within a decade or so of actually using them. She was 25 years away. She was paying for coverage against problems that wouldn’t be relevant for a quarter century.

Then there’s the fee drag. A 2.5% annual cost is particularly damaging over a long accumulation period because it works against the one thing a 40-year-old investor has most of: time. Compound growth is powerful over 25 years — but only if fees aren’t taking a cut of it every single year.

The tax treatment makes it worse. Variable annuity withdrawals are taxed as ordinary income in retirement. She hadn’t yet opened a Roth IRA — an account designed exactly for someone in her position, where growth and withdrawals are completely tax-free. She was being sold a more expensive product with less favorable tax treatment than one she hadn’t even used yet.

Annuities do have a time and a place. There are scenarios where they make genuine sense as part of a broader financial plan. This wasn’t one of them. An advisor acting in her best interest might have guided her toward a simpler, lower-cost starting point, or at minimum been honest that she wasn’t yet at a stage where a product this complex was the right fit. That honesty would have cost the advisor the business. It also would have been the right call.

It’s worth being clear: under the regulatory framework governing most advisors at the time, which held them to a suitability standard rather than a fiduciary one, this was a legal transaction. The product was suitable. The boxes were checked. But “suitable” and “in her best interest” were two different things, and the gap between them is exactly what the evolution toward Regulation Best Interest, which we covered earlier, was designed to address. The rules have moved in the right direction. They just hadn’t gotten there yet.

The client got a retirement account, technically what she asked for. What she didn’t get was an honest conversation about what actually made sense for her situation.

The pattern behind most of the stories people have heard about bad advisor experiences isn’t outright theft. It’s a relationship that was the wrong fit from the start, where nobody was willing to say so. Your job on the other side of any advisor conversation is equally simple: pay attention and ask questions. If something feels off, pay attention to it. The signals are worth trusting: being pushed toward a decision before you understand it, an advisor who can’t clearly explain how they get paid, leaving more confused than when you came in. Ask who their typical client is. Ask what kind of client they wouldn’t be a good fit for. An advisor who answers those questions directly, including the ones that might cost them your business, is showing you something. An advisor who hedges or redirects is showing you something too.

A few questions worth asking any advisor

Are you a fiduciary, and does that apply to everything you do for me? You already know why this one matters.

How do you get paid, specifically? Ask them to walk through their compensation across every service they might provide. The answer should be clear and comfortable to give. If it’s complicated or hedged, that’s information.

Who is your typical client, and who wouldn’t you be a good fit for? A direct question deserves a direct answer. The response tells you a lot about how they think about their practice.

Where we fit in, and where we don’t

Before those engineers could even ask whether I’d work with them, I told them who we’re built to serve. I led with it. Comprehensive advisory relationships make the most sense when there’s genuine complexity to justify the engagement. When income, equity compensation, taxes, and account structure interact in ways that benefit from active, ongoing oversight, the relationship produces real value. For someone in their first year of work, that inflection point usually hasn’t arrived. I was happy to answer their questions and point them in the right direction. But I wasn’t going to let them leave without knowing upfront that a full planning relationship at that stage would have been the wrong fit, and that I’d rather say so plainly than sign someone up for something that doesn’t serve them yet.

That’s the same honesty I’d want from any advisor. And it’s the standard we try to hold ourselves to at Stapleton.

We’re a fee-only RIA. We earn no commissions, sell no products, and are held to the fiduciary standard for everything we do. Our primary model is AUM-based. For clients who aren’t yet at that threshold but have the complexity that would genuinely benefit from working with a firm like ours, we offer a retainer arrangement that makes the relationship accessible at an earlier stage. I wrote about a real client situation back in Week 3 that illustrates exactly the kind of problem we spend our time on: one that developed quietly over years, invisible without someone actively looking across the full picture.

The clients who get the most from this kind of relationship tend to share a few things. They want advice that’s comprehensive, proactive, and genuinely personalized, not a product placement with a quarterly statement attached. And they’re oriented toward the long game: wealth built intentionally over time, not short-term optimization or performance chasing.

The clients who’ve gotten the most from this relationship tend to see us as more than advisors, and honestly, that’s how we see ourselves. Our conversations go beyond portfolios and plans. We talk about life: the career decision that’s been sitting with someone for months, the family goal worth building toward, the accomplishment worth pausing to acknowledge. We’re a sounding board and a consistent presence through the moments that matter. That kind of relationship is the most rewarding part of this work, and it’s part of what we’re looking for when we sit across the table from someone new.

We’re selective about fit, for the same reason we’re encouraging you to be. When we sit with a prospective client, we treat it as much like an interview on our end as on theirs. We want to understand what you’re actually looking for, what your financial life looks like, and whether this is genuinely the right match. If it is, we’ll tell you. If it isn’t, or isn’t yet, we’ll tell you that too.

That’s the same transparency we’ve been talking about throughout this piece. It’s the only honest way to start the right relationship.

Next week we return to the curriculum with a look at RSUs, the equity compensation that seems like a straightforward benefit until you realize how much it intersects with your taxes, your portfolio concentration, and the picture we’ve been building together.

If you want next week’s post in your inbox, subscribe here.

Josh

This post is educational and general in nature. Nothing here constitutes personalized investment or legal advice. Compensation structures, regulatory standards, and fee ranges vary by advisor, firm, registration, and jurisdiction. Fee ranges cited are illustrative approximations. Client situations described are anonymized. Readers should review any advisor’s Form ADV Part 2 for complete compensation disclosure.

Comments are closed