Taxes, Concentration, and the Planning Problem Nobody Connects for You

Week 6 | The Missing Chapter | Joshua Grass, CFA, CFP®

Your employer gave you RSUs. Did anyone explain what they actually do to your taxes, your portfolio, and your financial plan?

For most people, the answer is somewhere between “not really” and “not at all.” The grant shows up in an offer letter. Shares vest on schedule and land in a brokerage account. And the full picture tends to go unexplained: what that income means for your tax bill, how it fits into your investments, and what the sell-or-hold decision actually involves.

Restricted stock units have become one of the most common forms of compensation for high earners at public companies. Most people know what they are, roughly. What’s less well understood is how they function as a connected planning problem, one that touches your tax bracket, your investment concentration, and your account architecture all at once.

What actually happens when RSUs vest

Let’s start with the basics, because they’re worth stating clearly even if you’ve been getting grants for a few years.

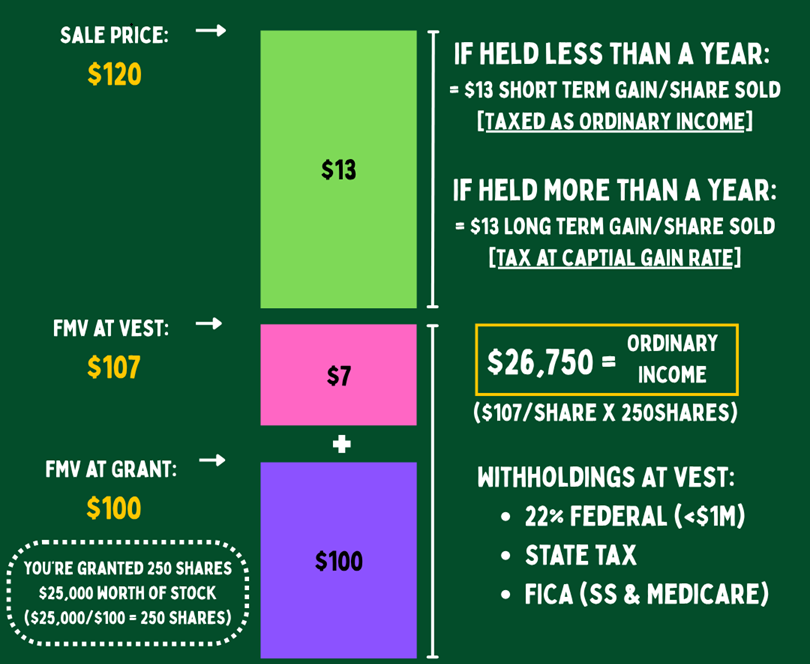

A restricted stock unit, or RSU, is a promise from your employer to give you shares of company stock after a certain condition is met, usually time. You’re granted a number of units on a specific date, but you don’t own anything yet. Those units vest over time, typically over four years, with common structures including 25% vesting per year or monthly vesting after an initial one-year cliff. When shares vest, the restriction lifts, the stock lands in your account, and something else happens at that exact moment: you have taxable income.

This is the part that surprises people. Most have a general sense that RSUs are taxable. The surprise is in the mechanics of when and how.

At the moment of vesting, the fair market value of the shares you receive is treated as ordinary income. The same character as your salary, sitting right on top of it. No special rate, no capital gains treatment. Your employer is required to withhold taxes on that income, and they do. What most people don’t know is that the withholding rate on RSU income is set by the IRS at a flat 22% for federal taxes. If your marginal federal tax rate is 22%, you’re covered. If your marginal rate is 32%, 35%, or 37%, you’re not. You’ll owe the difference when you file.

For most people earning $250,000 or more, 22% is a significant underestimate of what they actually owe. A $100,000 vest at 22% withholding generates $22,000 going to taxes at vesting. But if your marginal rate is 35%, the actual federal bill on that income is $35,000. That’s a $13,000 shortfall on a single vest, and that’s before state income taxes, which the withholding calculation may also underestimate.

The mechanism your company uses to cover the withholding is called “sell-to-cover.” On your vest date, a portion of your shares are automatically sold and the proceeds go toward the tax withholding. You receive the remaining shares. The instinct many people have is that because shares were sold and taxes were withheld, the tax obligation is settled. It isn’t. Sell-to-cover covers the statutory minimum your employer is required to withhold, not your actual liability. The difference follows you to April.

If you’ve been surprised by a tax bill in a year with significant vesting, this is almost certainly why. And if you have meaningful vests coming up and haven’t thought through the math yet, it’s worth doing before the year is out. The options are adjusting your W-4 withholding on your salary, making estimated quarterly tax payments, or setting aside cash specifically to cover the gap. None of those is complicated. The only bad version is being surprised.

The income-stacking problem

There’s a second tax issue that’s less obvious and, in some ways, more consequential over time: the way RSU income interacts with everything else on your return.

When RSUs vest, that income doesn’t show up in its own separate category. It shows up as ordinary income, stacked on top of your salary and any other compensation. And because the federal tax system uses marginal brackets, that stacking matters. The first dollars of income are taxed at lower rates; additional dollars push you progressively higher. If your salary already has you sitting near the top of the 24% bracket, a significant vest can push a substantial amount of income into the 32% or 35% bracket. The blended rate on the full vest ends up higher than the rate on any single dollar within it.

The stacking effect also touches things beyond your bracket. There are other thresholds that shift based on modified adjusted gross income: the ability to contribute directly to a Roth IRA, the net investment income tax, the additional Medicare surtax, and, for those approaching Medicare age, the beginning of IRMAA exposure. A vest that looks like a good problem to have in isolation can quietly trigger several of these at once when viewed in context.

This is one reason there’s an entire post coming on multi-year tax planning. The decision about how to handle a vest in a given year is often better made in the context of what the next two or three years look like. A year when income is lower, for any reason, is often a better year to absorb a larger vest or make other coordinated moves. A year when multiple income sources are already stacking is often the wrong time to add to that pile voluntarily. Knowing which year you’re in changes the calculus.

The sell-or-hold question

This is the one people ask most often, and it’s worth being honest that there isn’t a universal right answer. There is a framework for thinking about it, though.

When RSUs vest, the shares that land in your account are just stock. There’s no tax advantage to holding them versus selling them immediately. Unlike certain other equity instruments, there’s no preferential tax treatment waiting on the other side of a holding period at vesting. The income was recognized when the shares arrived regardless of what you do next. What you’re deciding from that point forward is a straightforward investment question: do you want to hold a position in your employer’s stock, or would you rather hold something else?

So ask yourself: would you buy this stock with cash today? Because that’s effectively what holding is, choosing to keep the position rather than selling it and redeploying elsewhere. If the answer is yes and it fits into your broader portfolio in a reasonable way, there may be a case for holding, at least in part. If you’ve held for more than a year from the vest date, a future sale would qualify for long-term capital gains rates rather than ordinary income rates. For most people in this income range, that’s a meaningful difference, typically 20% versus 37% on any gain above your cost basis.

The consideration that most often gets left out is concentration, and it tends to be the most consequential one.

The concentration problem you may not have named yet

Here’s a pattern that comes up regularly with clients who work at public companies: they have RSUs from their employer that vest and accumulate into a meaningful position in company stock. They also have a 401k that their employer matches, sometimes in company stock and sometimes into a target-date fund that happens to be overweight in the same sector. And they have a brokerage account with an S&P 500 index fund that may also carry exposure to the same company stock.

Three accounts. Three logins. And when you zoom out to see the whole picture, a significant concentration in one company’s fortunes and one sector’s performance.

That concentration is compounded by something that doesn’t show up in any brokerage account balance: your income. Your salary, your bonus, and your benefits all flow from the same employer whose stock you’re accumulating. Your career risk and your investment risk are sitting in the same place. If your company has a difficult year, your compensation, your equity value, and your portfolio can all take a hit simultaneously. That’s a different kind of risk than simply holding a large position in any single company.

How much employer stock is too much? There’s no bright line that applies to everyone, but the general principle most planners work from is that a single-stock position representing more than 10 to 15 percent of your investable net worth warrants a real conversation about the tradeoffs. The goal isn’t an automatic sell. That would ignore your tax situation, your conviction in the company, and the full financial picture. The goal is an honest look at the full exposure, including the career and income components, and a deliberate choice about how much concentration you’re comfortable carrying.

The question worth sitting with is simple: what would happen to your financial plan if your company stock declined significantly in the same year that your role was affected? A good plan doesn’t require that scenario to be probable. It just needs to be able to survive it.

A note on ESPPs

Many of the same people reading this also have access to an Employee Stock Purchase Plan, and it’s worth a moment here even though it deserves its own full treatment eventually.

An ESPP lets you purchase company stock through payroll deductions at a discount, often 15% below market price, and sometimes with a lookback provision that applies the discount to whichever price is lower: the price at the beginning or the end of the offering period. That structure can make the effective discount even larger in a rising market.

The tax treatment differs from RSUs and the mechanics vary by plan, so reading your specific plan documents matters. But the general principle is this: a 15% guaranteed discount is a very attractive return relative to most alternatives. If you’re not participating and your cash flow supports the payroll deduction, it’s usually worth a second look. The same concentration consideration applies, though. If you’re already accumulating significant employer stock through your RSU grants, the ESPP adds more exposure to the same underlying risk.

How this connects to the rest of the plan

We spent Week 3 building the three-bucket framework of taxable, tax-deferred, and tax-free accounts, and arguing that account architecture matters as much as what you’re invested in. RSUs are directly relevant to that architecture. The income lands in your taxable bucket by default, and the decisions you make around when to sell and what to do with the proceeds affect how your overall allocation evolves over time.

The ordinary income character of RSU vesting also means it interacts with the Roth contribution income limits, with the calculus around Roth conversions in lower-income years, and with the multi-year tax planning lens we’ll build out in Week 9. The specific moves available to you depend on your tax situation, your vesting schedule, and what else is happening in your financial life, which is precisely why equity compensation planning is most valuable when it’s connected to the rest of the plan rather than managed in isolation.

If you’re handling your RSUs, your 401k, and your brokerage account through three different portals with no one connecting them into a single picture, that’s the gap. It’s just a gap, and one that tends to make a lot of other decisions considerably clearer once you close it.

Josh

This post is educational and general in nature. Nothing here constitutes personalized investment or legal advice. Compensation structures, regulatory standards, and fee ranges vary by advisor, firm, registration, and jurisdiction. Fee ranges cited are illustrative approximations. Client situations described are anonymized. Readers should review any advisor’s Form ADV Part 2 for complete compensation disclosure.

Comments are closed