“The truth is rarely pure and never simple.”

-Oscar Wilde

On January 3rd, US forces captured Venezuelan President Nicolás Maduro, the man who had handed China control of roughly 80% of Venezuela’s crude exports. Markets barely budged. On February 28th, the US and Israel struck Iran, killing Supreme Leader Ali Khamenei and several of his senior military commanders. Brent crude jumped 15% in five days. The dollar (DXY) rose 1.4% in a week. The financial press covered both events as geopolitical news. I want to make the case that they were primarily financial operations executed with military tools, and that the target in both cases was the same: China’s most sophisticated weapon against the US dollar.

In Part One, I will focus on Venezuela and Iran, the two moves that have already happened. I will lay out the petrodollar thesis, walk through the data, acknowledge potential risks, and discuss the market implications. In Part Two, I will cover what I believe is the unspoken move in this strategy, one that dwarfs Venezuela and Iran in scale, and will dictate whether this was a futile endeavor.

I will not opine whether this is a good or bad strategy but merely try to put together a framework for why these decisions are intertwined and how the actions interrelate. I will not discuss any opinions on how “things are going” in Iran. As most of you have experienced, it is difficult to find the truth in news and social media with propaganda being facilitated by all sides of the equation. I would rather take a big picture view of the events and prepare for the good and the bad outcomes that could emerge.

Setting the Stage: The Petrodollar

In my August 2025 piece on the Triffin Dilemma and my January 2026 article on the Declining Dollar, I laid out the structural tension at the heart of US economic power: the dollar’s reserve currency status is not a birthright; it is a function of global energy pricing. Since the 1970s, oil has been priced in dollars. Countries must accumulate dollars to buy oil. They recycle those dollars into US Treasuries. This petrodollar loop is what allows the United States to run persistent deficits without triggering a sovereign debt crisis. If global energy trade migrates to the Chinese yuan, that loop breaks, and the ultimate question I keep returning to becomes much more urgent: when does the US have too much debt, lose investor confidence, destroy the dollar, and lose its reserve currency status?

China understood this architecture better than most. Beginning roughly a decade ago, Beijing quietly positioned itself to dismantle it, not through military confrontation, but through energy finance. It extended oil-for-loans arrangements to sanctioned energy producers, settled those trades in yuan rather than dollars, and built a growing shadow fleet infrastructure to move oil outside the visibility of Western financial systems. Venezuela and Iran were the two crown jewels of that strategy. Both are now severely disrupted.

Venezuela: More Than a Drug War

Operation “Absolute Resolve” on January 3rd was framed publicly around narco-terrorism, drug trafficking, and democracy. Those narratives are not wrong. Maduro was indeed indicted on narco-terrorism charges, and Venezuela has long been a hub for cocaine moving toward the United States. But if drug interdiction was the primary goal, a decade of sanctions and a $50 million reward on Maduro’s head should have been enough. Something else was part of the equation.

That something else is oil. Over the past decade, China became Venezuela’s dominant creditor and primary oil customer. Beijing extended $60 billion in loans backed by future oil payments through 2015. Venezuela was repaying that debt in barrels of oil, typically 50,000 to 100,000 barrels per day, at below-market prices. Much of this trade was settled in Chinese yuan, not US dollars. Venezuela was under US sanctions and had little choice but to accept the yuan. In doing so, it became a quiet but meaningful test case for China’s broader agenda to de-dollarize oil.

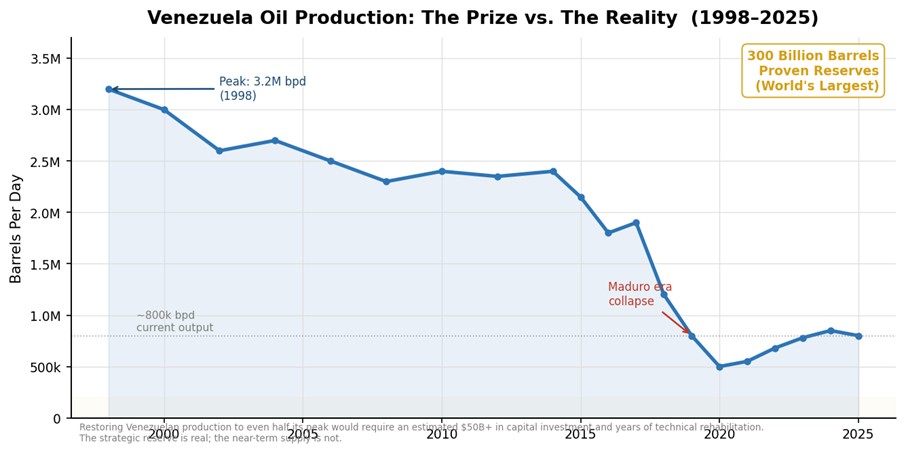

Figure 1: Venezuela oil production 1998-2025. The world’s largest proven reserves, chronically underproduced.

Venezuela has the world’s largest proven reserves, exceeding 300 billion barrels (~$30 trillion). As the chart above shows, Venezuela’s oil production collapsed from a peak of roughly 3.2-3.5 million barrels per day in 1998 to ~900,000 bpd today. The Maduro government destroyed the technical and financial capacity to extract it. China became Venezuela’s dominant creditor and primary oil buyer, purchasing the vast majority (~75–80% in recent periods) of its limited crude exports, often at steep discounts and settled outside the dollar system. From a purely financial lens, Venezuela was a Chinese-managed spigot of subsidized energy that also accumulated geopolitical debt. The US intervention severed that arrangement overnight. Venezuela’s acting government has since scrambled to reassure Beijing that Chinese investments remain secure, but US control over the energy sector and a new framework dictating how Venezuelan oil is sold and to whom fundamentally redraws the picture.

One important caveat: the $30 trillion strategic prize is long-term. The Venezuelan oil is thick and expensive to refine. Restoring Venezuelan production to even half its historical peak would require $50 billion+ in capital investment. The near-term supply will be modest. This is a decade-long play, not a 2026 story.

Iran: The Twelve-Day War and What Followed

The Iran story is more complex and a lot more dangerous. The June 2025 “Twelve-Day War” saw Israeli airstrikes followed by the US Air Force and Navy’s Operation Midnight Hammer on June 22nd, targeting the Fordow, Natanz, and Isfahan nuclear facilities with bunker-buster munitions. Nuclear talks were suspended. Protests erupted in Iranian cities in December over a collapsing rial and inflation of 50%+. Brief negotiations resumed in Geneva in February 2026, and then on February 28th, when those talks stalled, a second massive US-Israeli strike killed Supreme Leader Ayatollah Ali Khamenei along with multiple senior military commanders.

The stated justification was nuclear non-proliferation and regional security. But there is a parallel financial narrative that probably serves as the larger rationale. China was purchasing ~1.38 million barrels of Iranian oil per day in 2025, representing about 13% of its total oil imports, at a discount of $8 to $10 per barrel to market prices. This supply was paid predominantly in yuan and transported via shadow-fleet tankers specifically designed to bypass the dollar-based financial system. Iran had joined BRICS in 2024. The 2021 China-Iran “Comprehensive Strategic Partnership” promised $400 billion in Chinese investment over 25 years in exchange for preferred energy access. It was an alliance built explicitly around mutual dollar avoidance.

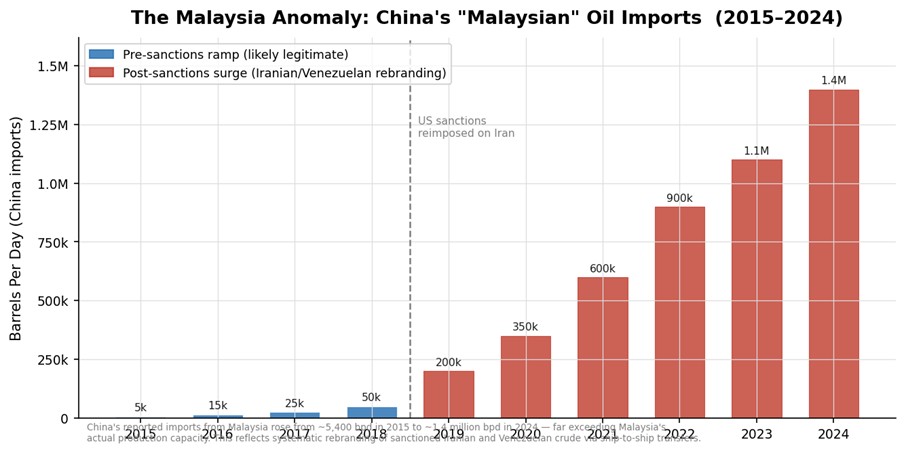

The scale of this arrangement becomes visible in a striking piece of data. Look at what happened to China’s reported oil imports from Malaysia:

Figure 2: China’s reported “Malaysian” oil imports, 2015-2024. Malaysia’s actual production capacity cannot explain this growth.

China’s reported imports from Malaysia rose from approximately 5,400 barrels per day in 2015 to roughly 1.4 million barrels per day in 2024. Malaysia’s domestic oil production is around 550,000 bpd total. This discrepancy has one explanation: systematic rebranding of Iranian and Venezuelan crude via ship-to-ship transfers in Malaysian waters, specifically engineered to evade US sanctions and avoid detection in Chinese customs data. The shadow fleet was not a marginal workaround. It was an industrial-scale operation.

That architecture is now severely damaged. The political relationship between Tehran and Beijing is highly uncertain. Beijing is scrambling to replace millions of barrels per day of discounted supply.

The Overarching Thesis: This Is About China

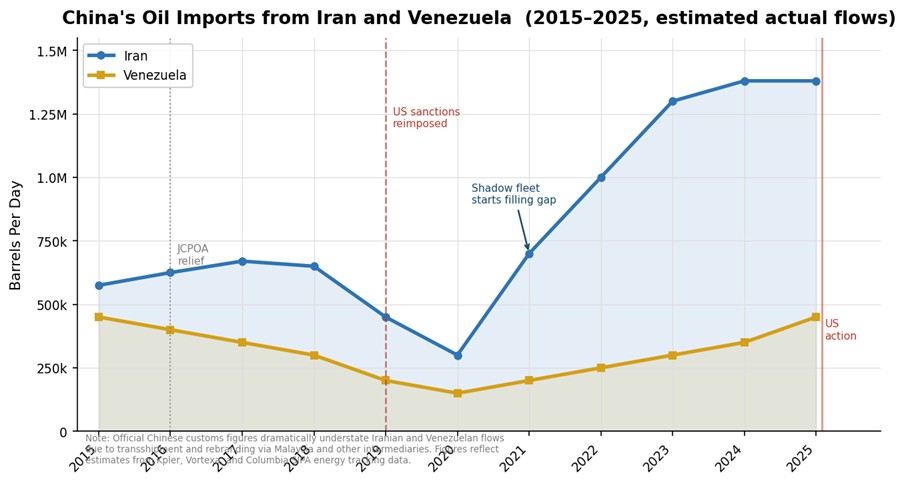

Figure 3: China’s actual oil imports from Iran and Venezuela, 2015-2025 (estimated). Combined: ~17% of China’s total supply, yuan-settled.

Let me be direct. I believe the primary connection between these two events and reason for military action is a deliberate strategy to exert financial pressure on China and shore up the petrodollar. China’s most dangerous economic weapon against the United States is not its military, its rare earth exports, or even its Treasury holdings. It is its systematic effort to conduct energy trade outside the US dollar, which underpins the dollar’s reserve-currency status.

China knew this and acted accordingly. Its investments in Venezuela and Iran were not “business as usual”; they were strategic positions in the architecture of dollar displacement. Venezuela provided collateralized, yuan-settled oil. Iran provided discounted, yuan-settled oil via shadow routes. Together, as the chart above shows, they represented roughly 17% of China’s total oil imports, discounted, yuan-denominated, and outside the petrodollar system. The US has now destroyed or severely disrupted both. Whether or not you agree with the legality or morality of these actions, the financial logic is precise.

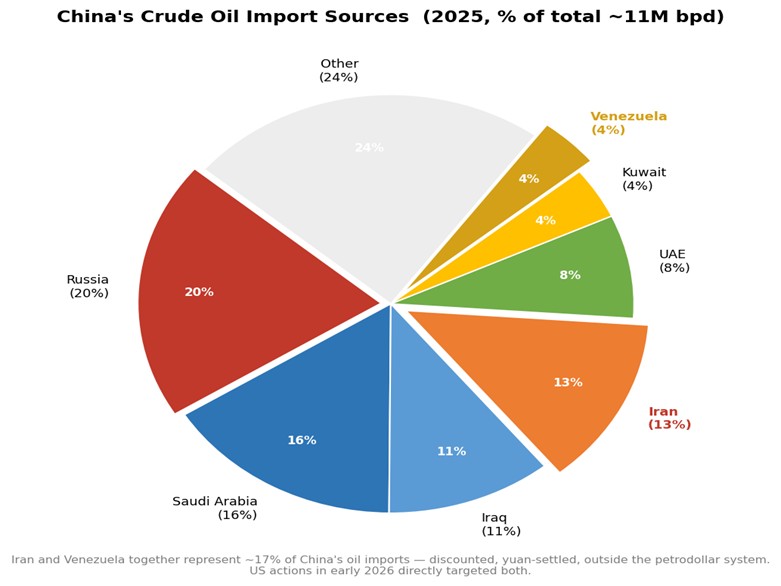

Figure 4: China’s crude oil import sources, 2025. Iran and Venezuela together: ~17%, all discounted and yuan-settled.

The Case for Secondary Benefits

The China/petrodollar thesis does not preclude genuine and altruistic benefits, and I think it is worth acknowledging them honestly.

- Freedom in Venezuela: Maduro oversaw one of the most brutal authoritarian collapses in modern Latin American history. Seven million Venezuelans fled the country. If the removal of his regime creates a genuine path toward democratic governance rather than a US-managed replacement, the human win is real.

- Dismantling Venezuela as a Narco-State and Cartel Safe Haven: Venezuela under Maduro was not simply a country with a drug problem; it was a country whose government was the drug operation.

- Democratic Opening in Iran: Iran’s population has been pushing back against the clerical regime for years, and the conditions for genuine change may now exist in a way they have not had since the revolution. Iran has a population of roughly 88 million with a median age of approximately 32 and a literacy rate exceeding 90%. It could become a great Middle Eastern country.

- Iranian nuclear non-proliferation: Iran was estimated to be weeks away from weapons-grade uranium enrichment capability. A world where that program is severely set back is objectively safer, regardless of the methods used.

- Middle East stability and oil flows: A weakened Iran means a weakened Hezbollah and Hamas. Gulf energy producers including Saudi Arabia, the UAE, and Kuwait operate in a more stable, less threatened environment. The global oil infrastructure becomes more reliably accessible.

- Long-term energy prices: A reconstruction of Venezuelan oil infrastructure under more competent management could eventually add significant supply to global markets, with deflationary consequences for energy prices over the next decade.

Where could this go wrong?

This strategy may accelerate de-dollarization rather than prevent it.

China and Russia are watching these events closely. The lesson they are drawing is not that they should use dollars, but that they need to accelerate their alternatives before the US dismantles them. China’s yuan-settled oil trade, while still a minority of global flows, has been growing steadily. Saudi Arabia has been quietly discussing yuan oil settlement. BRICS expansion continues.

Killing Khamenei may not end Iran’s nuclear ambitions.

History’s lesson from North Korea and Libya is clear: countries that give up or lack nuclear weapons face regime change. Countries that acquire them do not. Iran’s surviving leadership now has more incentive to develop nuclear weapons than before the strikes, not less. We may have bought some time, but potentially at the cost of a more determined nuclear adversary.

Short-term oil prices hurt domestic consumers.

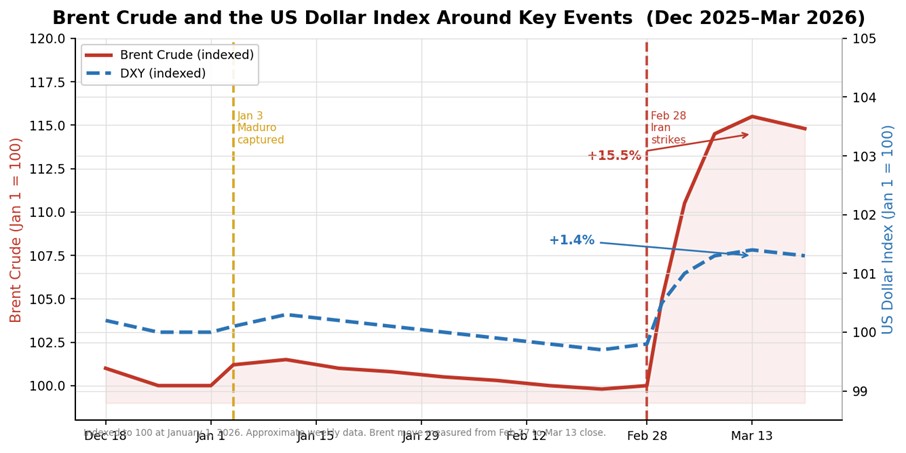

Brent crude rose over 15% in the week following the February 28th Iran strikes. A sustained move higher in oil prices is a domestic headwind: inflationary, consumer-punishing, and politically painful.

China has powerful tools of retaliation.

Disrupting China’s cheap oil supply is not a costless maneuver. China controls approximately 60 to 80% of global rare earth processing. Materials essential for defense systems, semiconductors, and the electric vehicle supply chain. It holds roughly $760 billion in US Treasuries. It could accelerate Taiwan tensions. The United States being busy in the Middle East could provide an opening for a strike. We have poked a very large bear.

Tail Risks

In addition to the concerns above, there are several tail risks:

- Broader Middle East flare-up: Iran has retaliated against Israeli and American targets in the region. A surviving Iranian regime, or Iranian proxies operating independently, could escalate in ways that disrupt Gulf oil flows, potentially the very outcome this strategy sought to prevent. The Strait of Hormuz handles approximately 21 million barrels of oil per day, roughly 20% of global supply.

- Global terrorist retaliation via proxies and inspired actors: Potential terrorist attacks around the world. Surviving IRGC Quds Force apparatus retains a decentralized global network capable of asymmetric retaliation far beyond the region

- Sovereign debt market disruption: If China were to begin aggressively selling US Treasuries as a form of economic retaliation, the effect on long-term yields could be severe. Combined with already-elevated deficit spending, this could produce a bond market dislocation that the Fed would be forced to address with renewed quantitative easing, reigniting the inflationary cycle.

- Venezuelan instability: Removing an authoritarian does not automatically produce stability or democracy. The Maduro regime’s structures remain largely intact under acting President Rodríguez. A protracted power vacuum or insurgency could disrupt any near-term oil production improvements.

Market Implications

Figure 5: Brent crude and the DXY around the Venezuela capture (Jan 3) and Iran strikes (Feb 28).

Potential Positives

- Dollar strength: The DXY rose ~ 1.4% in the week following the Iran strikes. If the petrodollar thesis plays out and global energy trade remains dollar-denominated, structural dollar demand is reinforced. This is supportive for US Treasuries, borrowing costs, and the Federal Reserve’s inflation-fighting credibility.

- Defense sector: Lockheed Martin, Raytheon, Northrop Grumman, and other defense companies are the obvious beneficiaries of elevated geopolitical tension and the demonstrated need to replenish inventories.

- US energy producers: Higher near-term oil prices, combined with potential Venezuelan production growth over the medium-to-long term, creates a positive environment for domestic producers. LNG exporters stand to benefit as buyers scramble for non-sanctioned supply.

Potential Negatives

- Oil price spike: The 15%+ oil price move since late February is a direct tax on consumers and businesses. If sustained, it complicates the Fed’s ability to cut rates and could reignite the stagflationary dynamics I discussed in my January article on the Declining Dollar.

- Equity market volatility: Geopolitical uncertainty is historically negative for risk assets in the short-to-medium term.

- Fixed income risk: If China retaliates through Treasury selling, long-term yields could rise sharply. The 10-year Treasury is a crowded safe-haven trade right now, but that trade can break quickly.

- Emerging market contagion: Countries that have been building trade and debt relationships with China face a fork in the road.

What Comes Next

Venezuela and Iran together represent roughly 17% of China’s oil supply. The disruption to Beijing’s discounted, yuan-settled energy architecture is real and material. But there is a number that should stop you: Russia supplies approximately 20% of China’s oil imports, all at deep discounts, increasingly settled in yuan since the 2022 Ukraine invasion. Russia is, by a considerable margin, the largest single yuan-settled oil pipeline in the world. And the strategy described in this note has not touched it.

In Part Two, I will make the case that Russia is not the missing piece of this strategy; it may be its most ambitious chapter. The outcome of whatever diplomatic process unfolds between Washington and Moscow in the coming months could determine whether the petrodollar strengthens or gets squeezed further over the coming decade. That conversation involves Russian demographics, rare earth minerals, European energy markets, and a geopolitical realignment that, if it succeeds, would make Venezuela and Iran look like opening moves.

Are we only delaying the decline and displacement of the US dollar as the reserve currency?

No responses yet