Week 4 – The Missing Chapter – Joshua Grass, CFA, CFP®

Our son Beaux was born on December 4th, three weeks ahead of schedule.

A few weeks later, the medical bills arrived. We paid them and didn’t touch the HSA.

I want to be honest about what made that an easy call for us. We’re in a financial position where we can afford to contribute to an HSA consistently. We have good insurance that covered the significant majority of the delivery costs. And even if we’d been on the hook for our full annual out-of-pocket maximum, we could have covered that from our regular cash flow without real strain. That’s not a universal position, and I don’t want to gloss over it. For a lot of people, the HSA functions as exactly what it sounds like: a savings buffer for healthcare costs that insurance doesn’t cover. A way to handle an unexpected bill without disrupting everything else. That’s a completely legitimate and useful thing for it to be.

But at our house, we think about the HSA differently. The mentality is straightforward: this money is more efficient if you let it sit and grow, and draw on it strategically later rather than spending it as bills come in. It’s a frame I find myself walking clients through regularly.

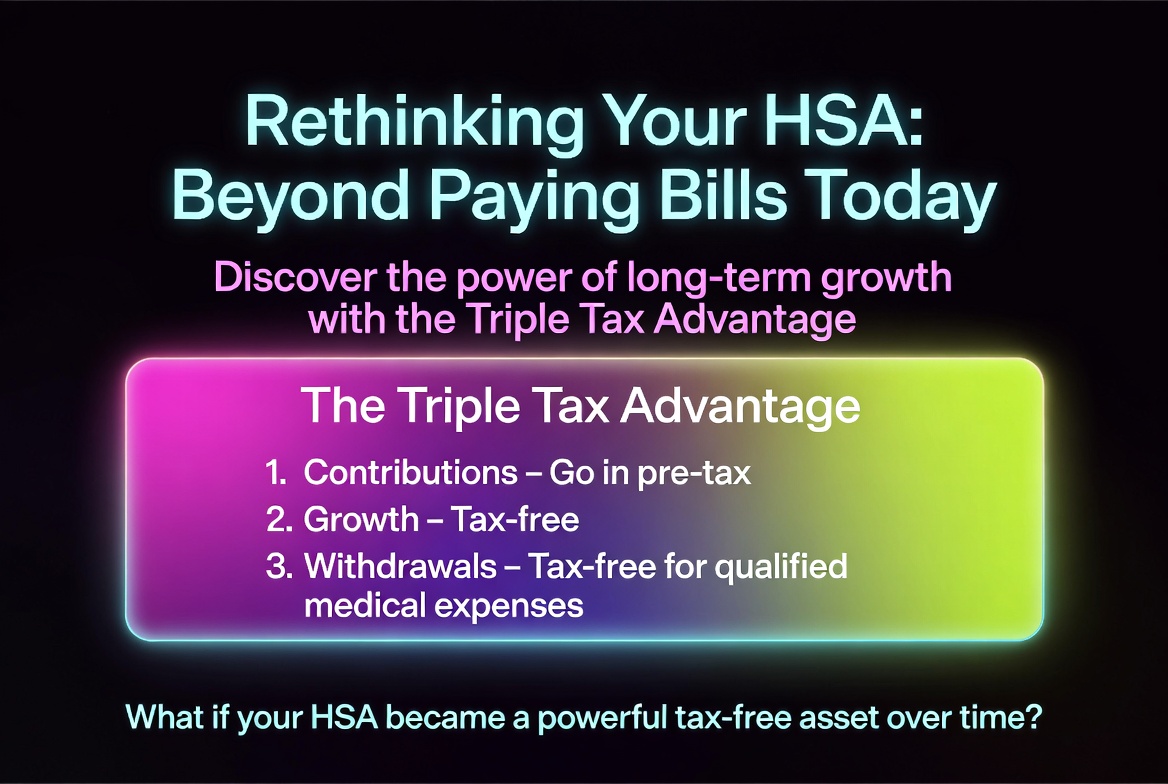

The only account that does all three

Let me be specific, because the specifics are what make this interesting.

Most tax-advantaged accounts give you one or two of the following: a tax break on contributions, tax-free growth, or tax-free withdrawals. The HSA gives you all three simultaneously, and it is the only account in the entire tax code that does.

Contributions go in pre-tax. If you contribute through payroll deduction, those dollars come out before federal income tax, state income tax, and FICA taxes, the 7.65% that covers Social Security and Medicare. That last part is one most people don’t know. Your traditional 401(k) is also pre-tax, but FICA still applies before those contributions leave your paycheck. The HSA skips FICA entirely. Depending on your income level, that alone is a meaningful advantage that doesn’t show up in most comparisons.

Growth is tax-free. Any money invested inside your HSA compounds without being taxed annually. No taxes on dividends. No capital gains when you rebalance.

Withdrawals for qualified medical expenses are tax-free. When the money comes out for healthcare, whether today or twenty years from now, it comes out without a tax bill attached.

If you’re building the architecture we laid out in Week 3, the HSA is your most powerful tool for the tax-free bucket. It beats the Roth IRA on the tax math because contributions avoid FICA. And unlike the Roth IRA, there is no income limit. The HSA is available to anyone enrolled in a qualifying high-deductible health plan, regardless of how much they earn.

The mechanic most people never use

Here is where the thinking can shift.

Every time you use HSA money to pay a medical bill, you are spending tax-advantaged dollars today, dollars that would otherwise compound tax-free for years, potentially decades. That is a tradeoff. Not always the wrong one, but a tradeoff worth understanding.

The IRS does not require you to reimburse yourself from your HSA in the same year you incur the expense. There is no time limit on reimbursements. You can pay a medical bill out of pocket today, keep the receipt as documentation, and reimburse yourself from your HSA years later, after the money has had time to grow.

What that looks like in practice: a $3,000 medical expense, paid from checking today, becomes a $3,000 documented receipt. The $3,000 that stays in your HSA, invested and compounding tax-free, could be worth considerably more by the time you draw it down. When you eventually reimburse yourself, the full amount comes out tax-free. You paid the bill from your checking account in the present. You receive a tax-free distribution from your HSA in the future.

This is sometimes called the “receipt strategy,” and it is completely legitimate as long as you have documentation for the underlying expense and you incurred the expense while the HSA was active.

Now, I’ll be the first to admit: the idea of keeping receipts for 30 or 40 years sounds like its own kind of nightmare. The one that went through the wash in your pants pocket. The one you forgot to ask for. The mile-long Walgreens receipt you were not about to fold up and file anywhere. And before you say “receipts are digital now.” Sure, some are. Which means they’re scattered across your email, your pharmacy app, a patient portal you haven’t logged into since 2019, and whatever cloud storage service you signed up for, uploaded three things to, and then forgot the password to while paying $9.99 a month for it. But if meticulous decades-long recordkeeping isn’t exactly your vision of a well-lived life, there’s a practical backup worth knowing about: Medicare premiums. Starting at 65, your Medicare Part B and Part D premiums are qualified HSA expenses, meaning you can pay them directly from your HSA, tax-free, no old receipts required. For most retirees, that’s a meaningful qualified expense showing up year after year, and a clean way to draw the account down without needing a paper trail that dates back to your 30s.

This approach requires being able to pay medical bills out of pocket without real strain, and not everyone is there yet. If using the HSA to cover current expenses is what keeps your cash flow intact, that’s the account doing exactly what it should. A worthwhile goal from here is building enough of a financial buffer that eventually you have the option to think about it differently. The receipt strategy gets more powerful the longer the balance is left to grow.

What happens at 65

Most people know the basics of the HSA spending rules. Fewer know what happens on the other end.

Before age 65, if you withdraw from your HSA for something that doesn’t qualify as a medical expense, you owe income tax on the withdrawal plus a 20% penalty. It is genuinely punitive, which is part of why people treat the HSA with such caution.

After age 65, the penalty disappears. Non-medical withdrawals from an HSA are simply taxed as ordinary income, the same as withdrawals from a traditional 401(k) or IRA. No penalty. Just ordinary income tax.

What that means, functionally, is that your HSA is a bonus retirement account. Used for healthcare, it is entirely tax-free, and healthcare costs in retirement are large, predictable, and something most retirement projections underestimate. Fidelity’s most recent estimate puts the average retiree’s healthcare costs at roughly $165,000 per person in retirement, not counting long-term care. An HSA that has been growing tax-free for decades is a meaningful asset against that number.

If you don’t use it all for healthcare, the balance just becomes a traditional-IRA-equivalent: taxable on withdrawal, but accessible for anything you want. You lose the tax-free advantage for non-medical withdrawals, but you never lose the tax-free growth, and you never face the early withdrawal penalty again.

There is no other account that works this way.

A few details worth understanding

The HSA has requirements that are worth knowing before assuming you have access to it.

To contribute, you must be enrolled in a qualifying High Deductible Health Plan, an HDHP. Not all employer plans qualify. If your employer offers multiple insurance options during open enrollment, check whether yours is HSA-eligible; it will typically be labeled clearly if it is.

In 2025, the contribution limits are $4,300 for individual coverage and $8,550 for family coverage. If you’re 55 or older, there is a $1,000 catch-up contribution available, following the same pattern as retirement accounts.

The other thing most people don’t realize: the money in your HSA does not have to sit in a cash account. Most HSA providers offer an investment option once your balance clears a certain threshold, typically a few hundred to a couple thousand dollars. Above that threshold, you can invest the rest in mutual funds or index funds, the same way you would in a brokerage or 401(k). The growth is what makes the long-term math interesting. A cash balance earns almost nothing. An invested balance compounds tax-free, and that difference accumulates significantly over time.

If you have an HSA and you’ve never looked at whether the investment option is available to you, that is worth a few minutes to check.

The question underneath the decision

When the bill came after Beaux was born, the choice was clear for us. But honestly, it was never really about that particular bill. It was about how we think about the account. Not as a medical spending fund with some tax advantages attached, but as a tax-free investment vehicle that also happens to be available for healthcare when we need it. That framing changes whether you look for the investment option, whether you reach for it every time a bill arrives, or whether you stop and think first about what makes more sense.

Not everyone is in a position to let it sit and grow. That is real, and it is not a failure. The goal is not to leave the HSA untouched as a matter of principle. The goal is to understand what you are working with and make a deliberate choice rather than a default one.

If you want next week’s post in your inbox, subscribe here.

Josh

Joshua Grass, CFA, CFP® is a financial advisor at Stapleton Asset Management. This blog is educational content and does not constitute personalized investment, tax, or financial planning advice. The 2025 HSA contribution limits referenced are current as of the publication date and are subject to annual IRS adjustment. Consult a qualified tax or financial planning professional for advice specific to your situation.

Comments are closed