In my September 2025 article, “Addressing Global Trade Imbalances: Policy Insights and the Triffin Dilemma“, I explored the structural challenges facing the global economy, with a particular focus on the overvalued U.S. dollar due to its status as the global reserve currency. I highlighted how the dollar’s strength exacerbates trade deficits by making American exports less competitive while encouraging imports. This ties directly to the Triffin Dilemma, the inherent conflict in which the United States, as the issuer of the world’s reserve currency, must run persistent deficits to supply global liquidity, yet those deficits erode confidence in the dollar over time. I argued that policy measures can try to address these imbalances, including targeted interventions to lower the dollar’s value while trying not to trigger market instability. Truly a tight rope balancing act…

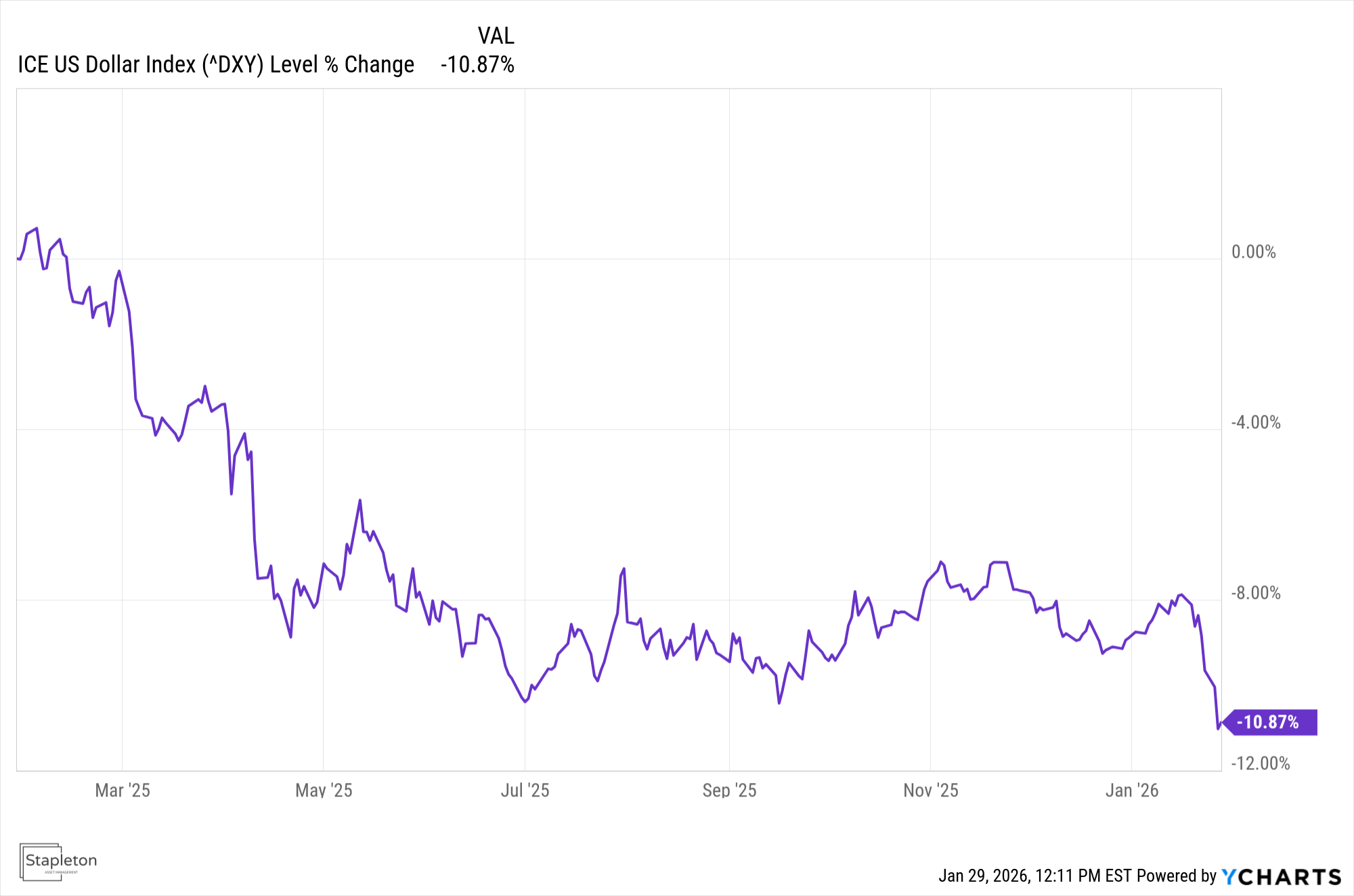

The U.S. Dollar Index (DXY) has declined about 11% during the last year, driven by Fed policy expectations/unpredictability, debt/deficit concerns, and trade policy uncertainty:

Figure 1 – Recent drop in the dollar, but about 11% decline since Trump took office

Meanwhile, precious metals have surged as investors seek hedges against currency depreciation and inflation. Silver has climbed an astonishing 175% since my September article, rising from about $41 per ounce to over $113 per ounce. Gold has also jumped, from roughly $3,550 per ounce to around $5,350 per ounce, a gain of over 50%. These movements underscore a pivotal theme: the current administration wants a weaker dollar to revitalize its export sector and rebalance global trade.

Figure 2 – Gold and Silver have been on a tear over the last year

Why does the Administration want a Weaker Dollar?

At its core, a depreciating dollar makes American goods and services more affordable on the international stage. When the dollar weakens, foreign buyers can purchase more U.S. products with their local currencies, boosting demand for everything from agricultural commodities to manufactured goods and technology. This is particularly desirable in addressing the chronic trade deficits I discussed in my prior article. The Triffin Dilemma suggests that an overvalued dollar perpetuates these imbalances by incentivizing the U.S. to import more while exporting less, flooding the world with dollars but undermining confidence and long-term stability.

A couple days ago, President Trump reinforced the case for embracing dollar weakness. When he was confronted about the US dollar decline, he stated, “No, I think it’s great… the value of the dollar — look at the business we’re doing. The dollar’s doing great.” He has long argued that a weaker dollar enhances competitiveness: “It doesn’t sound good, but you make a hell of a lot more money with a weaker dollar… than you do with a strong dollar.” This view aligns with his administration’s focus on tariffs and trade deals to protect U.S. industries, viewing currency depreciation as another tool to “sell more goods internationally.”

The surge in precious metals like silver and gold further signals market anticipation of this shift. Investors are flooding into these assets as safe havens amid dollar weakness, viewing them as inflation-protected stores of value. Silver’s massive rally reflects not just speculation, but also industrial demand tied to AI/energy production as well as supply constraints and short squeezes.

Beyond exports, a depreciating dollar offers a few other positives:

- Boost to Manufacturing and Employment: Lower export prices can stimulate production, leading to factory expansions and hiring. This aligns with efforts to reshore supply chains and reduce reliance on foreign manufacturing.

- Tourism and Services: A cheaper dollar attracts more international visitors and supports service exports like education and entertainment.

- Corporate Earnings: Multinational firms with overseas revenues benefit when converting foreign earnings back to dollars, potentially supporting stock market performance.

Unfortunately, there are risks and negative outcomes associated with a lower dollar as well:

- Higher Import Costs: The flip side of cheaper exports is pricier imports. Everyday goods like electronics, apparel, and oil become more expensive, squeezing household budgets and contributing to cost-push inflation.

- Reduced Purchasing Power: Americans’ global buying power diminishes, affecting everything from vacations abroad to investments in foreign assets.

- Capital Flight Risks: A persistently weak dollar may reduce foreign investment in U.S. Treasuries and equities, as returns erode when converted back to stronger currencies.

The most pressing concerns revolve around inflation and interest rates. A depreciating dollar amplifies inflationary pressures by raising the cost of imported inputs, which could cascade through supply chains. If inflation accelerates, which could be stoked by additional fiscal stimulus, the Federal Reserve may respond with higher interest rates to try to keep inflation in its box. While this could stabilize inflation, it might slow down the economy, increase borrowing costs for businesses and consumers, and potentially trigger a recession. As outlined in the Triffin Dilemma, unchecked deficits to support global liquidity can lead to inflationary spirals, erode confidence in the dollar, and require painful spending cuts and higher interest rates.

Japan’s Financial Turmoil: Echoes of the Yen Carry Trade Unwind

As I detailed in my article “The Unwind of the Yen Carry Trade: Understanding the Reverse Carry Trade and Its Global Consequences“, borrowing cheaply in yen to invest in higher-yielding assets abroad has long fueled global liquidity, but it also carries risks. When Japanese yields rise or the yen strengthens quickly, it forces an unwind, leading to asset sales worldwide and market volatility. This scenario has been unfolding since the start of 2026.

Japan’s bond yields have reached historic highs, with the 40-year Japanese Government Bond (JGB) rising to 4.25% and the 10-year yield rising to 2.35%, up from 1.00% a year ago. This rate move, along with pledges for aggressive fiscal expansion, has compelled the Bank of Japan (BOJ) to raise rates to 0.75% in December 2025, the highest in 30 years.

The yen has also weakened and hit a peak of 160 against the dollar, which prompted US and Japan to intervene. The rising Japanese yields force repatriation of funds, which can spark rapid and large sales of US Treasuries and US stocks, especially tech stocks.

Broader Implications for Global Fiat Currencies and Central Bank Policies

The dollar’s decline, compounded by Japan’s yen woes, raises many questions about fiat currencies in general. Persistent currency depreciation erodes trust in paper (fiat) money, as seen in historical episodes where over-issuance led to hyperinflation or shifts to alternative stores of value, such as gold. In our current environment, with major developed economies running high deficits and facing demographic pressures, fiat systems are stressed. The Triffin Dilemma extends beyond the dollar: reserve currencies like the euro and yen face similar tensions, where providing global liquidity conflicts with domestic stability.

Central banks may respond with further quantitative easing to add liquidity and keep yields capped, as the BOJ has done since the 1990s. More QE risks fueling more asset bubbles and exacerbating wealth inequality while delaying necessary spending cuts. If Japan’s bond shock triggers a full yen carry trade unwind, it could force repatriation and liquidity crunches elsewhere, prompting the Fed, ECB, or others to expand balance sheets again. This “race to the bottom” in currency values might accelerate de-dollarization trends, with nations like China or BRICS members pushing alternatives.

Conclusion: What Next?

A weaker dollar has a direct, upward effect on commodity prices denominated in USD. Since commodities such as oil, natural gas, copper, steel, platinum, palladium, agricultural goods, and others are priced globally in dollars. A depreciating currency means it takes more dollars to buy the same quantity, pushing nominal prices higher. This massive run-up in gold and silver could signal that we are entering a new commodity bull market driven by inflationary fears, declining fiat currencies, and new quantitative easing programs. The AI/tech capital expenditure explosion could also drive further demand for commodities to build the infrastructure and produce the required electricity.

It is not clear whether the Trump Administration’s desire to reshore manufacturing into America will work, but it does seem like inflation is here to stay. Congress has made no significant cuts to mandatory programs, and cuts look unlikely to happen soon. US equity valuations are lofty, but inflation could create an unnatural floor in equity prices, as companies are valued by a declining USD. Sometimes the best investment strategy is to preserve real wealth rather than chase growth stories. This seems to be one of those times.

Comments are closed