“The truth is rarely pure and never simple.” -Oscar Wilde On January 3rd, US forces captured Venezuelan President Nicolás Maduro, the man who had handed China control of roughly 80% of Venezuela’s crude exports. Markets barely budged. On February 28th, the US and Israel struck Iran, killing Supreme Leader Ali Khamenei and several of his senior military commanders. Brent crude jumped 15% in five days. The dollar (DXY) rose 1.4% in a week. The financial press covered both events as geopolitical news. I want to make the case that they were primarily financial operations executed with military tools, and that the target in both cases was the same: China’s most sophisticated weapon against the US dollar. In Part One, I will focus on Venezuela and Iran, the two moves that have already happened. I […]

In my September 2025 article, “Addressing Global Trade Imbalances: Policy Insights and the Triffin Dilemma“, I explored the structural challenges facing the global economy, with a particular focus on the overvalued U.S. dollar due to its status as the global reserve currency. I highlighted how the dollar’s strength exacerbates trade deficits by making American exports less competitive while encouraging imports. This ties directly to the Triffin Dilemma, the inherent conflict in which the United States, as the issuer of the world’s reserve currency, must run persistent deficits to supply global liquidity, yet those deficits erode confidence in the dollar over time. I argued that policy measures can try to address these imbalances, including targeted interventions to lower the dollar’s value while trying not to trigger market instability. Truly a tight rope balancing act… The U.S. Dollar Index (DXY) has declined about 11% during the last year, driven by Fed […]

Introduction Over a year ago, we explained how the Japanese Yen Carry Trade works, and now we need to examine its implications as Japan has experienced significant market dislocation. After more than 25 years of ultra-low (and at times negative) interest rates in Japan, the Bank of Japan (BOJ) has finally begun a genuine normalization cycle. The BOJ raised its policy rate to 0.50% in January 2025, the highest level since 2008, and has made clear that further hikes are coming, with a 25 basis point increase to 0.75% expected at the December 2025 meeting as inflation remains above target and wage growth continues at the fastest pace in three decades. Japan’s core inflation rate rose to 3% in October 2025, marking the sharpest increase in three months and staying above the BOJ’s 2% target for the 43rd consecutive month. Meanwhile, nominal hourly wages rose 3.5% year over year […]

Over-Valued Dollar The recent excitement has been about pressure on the Federal Reserve to lower the Fed Fund’s rate. I addressed it primarily in “Interest Rates and Tariffs: Putting Numbers Into Perspective”. My conclusion was that it is an important tool amongst many, but not a one-stop solution. I addressed “Tariffs, Trade Deficits, and Government Debt” trying to distill how all of these pieces are interrelated. Now we should add a component that is the elephant in the room, the strength in the US Dollar The core issue at hand is the persistent overvaluation of the U.S. dollar, which perpetuates trade deficits and undermines domestic manufacturing competitiveness. This overvaluation stems from the dollar’s status as the global reserve currency—a phenomenon known as the Triffin Dilemma. The Triffin Dilemma, named after economist Robert Triffin, refers to the conflict of interest faced by a country whose currency serves as the global […]

Market Euphoria US equity market valuations have experienced remarkable market cap appreciation and resilience to downdrafts. The headline news attributes it to technological innovation, low interest rates, and fiscal stimulus. Is it real, or are we experiencing a tech bubble that has, by some metrics, surpassed what we saw in the dot com bubble of the late 90’s? Key valuation metrics suggest that US stocks, particularly in technology-heavy indices, are trading at extended levels. Will Artificial Intelligence (AI) deliver, or are we repeating our past mistakes of over-estimating the immediate benefits of a ground-breaking technology and getting ahead of ourselves? Concentration in the S&P 500: Dominance of NVDA and MSFT The S&P 500 is market-cap weighted, meaning larger companies exert outsized influence in the S&P 500’s returns. As of August 14, 2025, the S&P 500’s total market capitalization is approximately $54.45 trillion. About a year ago, I showed that […]

Federal Reserve As the Federal Open Market Committee (FOMC) prepares for its July 29-30, 2025 meeting, we are all closely watching for any signals on interest rate policy. The current federal funds target range stands at 4.25% to 4.50%, with the effective rate hovering around 4.33%. The FOMC’s July session is widely anticipated to result in no change to the current rate range, with market consensus pointing to a 96.9% probability of holding steady. According to the CME FedWatch Tool, there’s only a slim 3.1% chance of a 25-basis-point (0.25%) cut, reflecting caution from the Federal Reserve as it assesses incoming data on inflation and employment. This cautious stance has been rationalized by the FOMC due to concerns about inflation from the impact of tariffs on prices. So far, that fear has not materialized and we will see if the additional tariffs starting on August 1 will spark the […]

The Surge in U.S. Treasury Yields In recent weeks, the U.S. Treasury market has experienced significant volatility, with the 10-year Treasury yield climbing to 4.535% and the 30-year yield reaching 5.008%, levels not seen since April and November 2023, respectively. This sharp increase, which saw the 10-year yield rise from below 4% to around 4.5% in a matter of days which is aligned with our thought that debt levels, trade deficits and government spending have been on an unsustainable path. This could be the start of something larger which could have an impact on global markets in weeks and months to come. What’s Driving the Increase? Several factors are contributing to this bond market upheaval: Trade War and Tariff Policies: The announcement of broad tariffs by the Trump administration, including a 25% tariff on foreign-made cars, has fueled market uncertainty. Tariffs are expected to increase inflationary pressures by […]

Tariffs are the topic du jour. As I said on April 4th, Trump has put the global economy on track for a global recession. We are currently waiting to see what responses and “deals” are made between countries in regards to tariffs, so we most likely have many weeks and probably months before we know what the global trade playing field looks like. While there is significant focus on tariffs, less attention is paid to how tariffs and trade deficits are interconnected, and even less to how trade deficits influence government debt and economic strength. These issues are complex, but I will attempt to simplify the framework and untangle the web. Part 1: The Basics of Trade Deficits and Government Debt What Is a Trade Deficit? Imagine you’re shopping and spending more money than you’re earning (like most Americans). A country does something similar when it has a […]

In early 2025, the Department of Government Efficiency (DOGE), spearheaded by Elon Musk, has been touted as a potential game-changer for tackling wasteful federal spending. Most Americans support the idea of dramatically cutting the federal government’s size and scope, but the elephant in the room is not being addressed. DOGE’s reported estimated savings of $115 billion (NPV) so far pale in comparison to the scale of the U.S. fiscal challenge. With the national debt exceeding $36.6 trillion and annual interest expenses alone over $1 trillion, DOGE’s initial efforts are a step in the right direction but represent less than 1/3 of 1% of the current debt. We are talking about current debts, but the massive issue is the exponentially growing debt in the future. To actually balance the budget and stabilize the debt-to-GDP ratio at 100% for the foreseeable future, extraordinary measures are required. DOGE’s Limited Scope in the […]

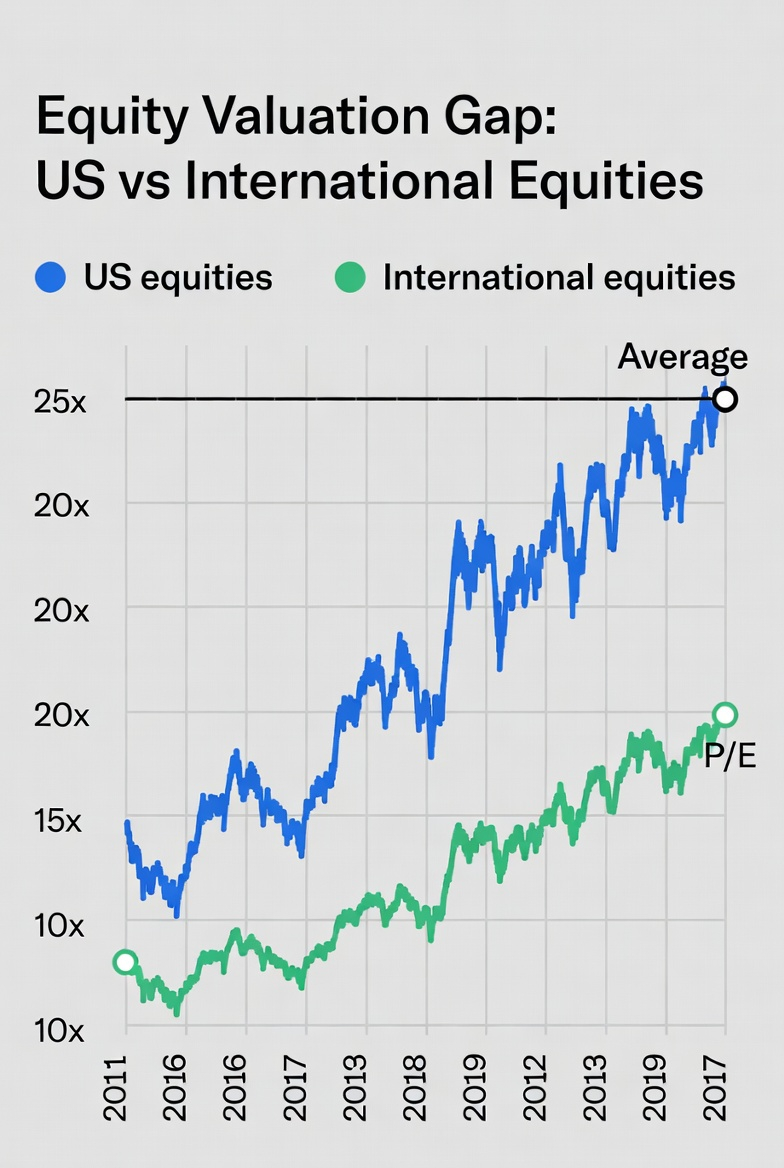

US stocks have reached a 75-year high in their relative valuation compared to the rest of the world, surpassing even the peaks seen during the infamous dot-com bubble and the Nifty Fifty era of the 1970s. Since the early 2000s, especially post-2008 financial crisis, US equities have consistently outperformed global markets, reaching levels not seen since the dot-com bubble at the turn of the millennium. This trend has only accelerated in recent years, with the US market trading at over 2 standard deviations above its long-term mean relative to global equities. What is driving this difference and is it sustainable? Just How High are US Equity Valuations? There are a few market valuation metrics that I find useful for broader market valuation. The first is the CAPE (cyclically adjusted price-to-earnings) Shiller ratio for the S&P 500. It represents the current S&P 500 Index Price / 10-Year Average Inflation-Adjusted Earnings. […]